I own very few biotech or pharma stocks. I heard the boys on The Compound talking about going long Pfizer recently, and so I thought it would be worth a look.

The Pfizer comment was casually dropped toward the end of this episode of The Compound with Friends with JC Parets and Joe Fahmy as guests. If you listen to finance podcasts, the shows from The Compound are great. This episode was a lot of fun and also contained some good tips on gauging the market trend and then how to adjust your trading or investing.

JC Parets is a “technician” focused on charts and price action. So I’ll share a couple charts. Here’s the past year, showing the stock’s decline and what might be a bottom forming.

Zooming out to the 5 year view, you can see that the recent bounce is off pre-COVID support levels.

My usual process for investing in a stock is to (1) figure out if the company is exceptional, (2) make sure the management is strong, (3) figure out a fair value price, then (4) check the technicals for good entry and exist points.

This post is a kind of stream of consciousness dive into a company I haven’t really looked into deeply before. I’m going to scan through some fundamental numbers and a bit of news to get a feel for the market sentiment. Then I’ll read some earnings reports, watch some earnings calls and interviews with the management, dive deeper into the fundamentals, and try to figure out 1-3 above there.

I haven’t looked into Pfizer in a long long time. I just know that it rallied decently through COVID because of their vaccine, but has tanked in the past 1-2 years. This is a similar story to a lot of stocks that boomed and busted through COVID. Sure the COVID related sales are shrinking, but are we really to believe that Pfizer is a less valuable company than it was 3 years ago before any of the COVID stuff even happened?

Is Pfizer a good value play now? Let’s take a look.

Okay, some high level numbers.

-

Share price at close January 8, 2024: $29.58

-

Market Cap: $166.4 Billion

-

PE: 16.19

-

PS: 2.43

So notably here the PE is below average for the S&P, and the PS is average for the S&P. To me, this means the market views Pfizer as a relatively boring company with limited growth. As a rule of thumb, I tend to use 15 PE and 2x sales as conservative numbers for mature companies in my forecasts… it’s kind of the minimum the typical healthy company should trade at.

So what’s up with Pfizer? How is their drug pipeline? Are some of their big money makers going generic?

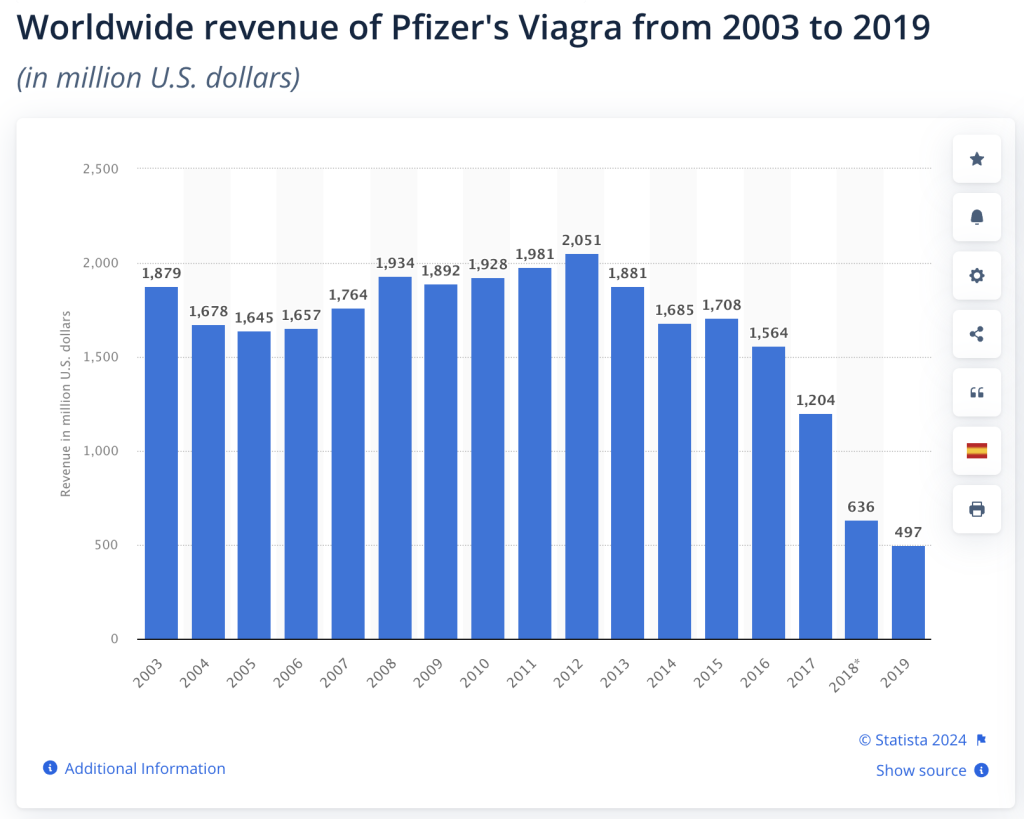

For example, I know from many a podcast ad that generic options of Viagra are available. Here is a chart from Statista.com showing revenue from Viagra sales, down pretty sharply from a high of $2B in 2012 to $497 million now.

I’m digging into some news now, not to build an investment thesis for Pfizer, but to get an idea for the market sentiment. I’m trying to figure out why the stock is down ~50% the past 2 years. Then I’ll dig into the historic numbers, listen to some earnings calls, maybe build my own model, and figure out if the company is worth investing in and if so at what price.

But anyway, here’s some recent news that pops up when I search for “Pfizer drug pipeline” and “Pfizer drugs going generic”/etc.

Here’s an article by Nadia Bey at BioSpace about 9 of the biggest drugs that lost exclusivity last year. Pfizer’s drug Eraxis (an antifungal drug) is on the list. The article, however, actually has a good quote for Pfizer:

Not every company will experience this decline in the same way. For example, Eraxis, an antifungal drug owned by Pfizer, is expected to lose its exclusivity in September. But loss of exclusivity probably won’t have a major impact on the company, said S. Sean Tu, a law professor at West Virginia University and affiliated faculty at Harvard Medical School’s Program on Regulation, Therapeutics and Law.

“Even if a lot of generics [for Eraxis] went on the market tomorrow, I don’t think it would hurt Pfizer’s bottom line. They have a pretty diverse portfolio,” Tu told BioSpace.

They have a diverse portfolio. Pfizer had $100B in sales in 2022. I’m taking a note to figure out how much of that was from the COVID related drugs, but basically no one or few drugs makes up Pfizer’s entire pipeline. Plus Pfizer sells generic drugs themselves. Are they able to position themselves to benefit more from generics than they lose?

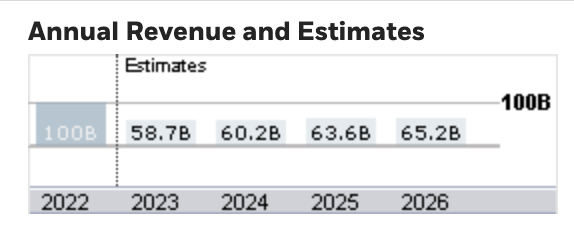

Quick aside before digging into some more articles. When I looked up that revenue number, I saw full damage to the stock. Those 2022 revenue numbers (boosted by COVID related sales, which we will dive into) are estimated to be cut nearly in half in 2023.

I often check out these revenue and earnings estimates in Etrade. They pull numbers from many sources. And while I like to do my own research to come up with my own numbers, it’s nice as a quick glance at what the market expects and kind of the middle path forward for the stock. These charts are not good, no buno.

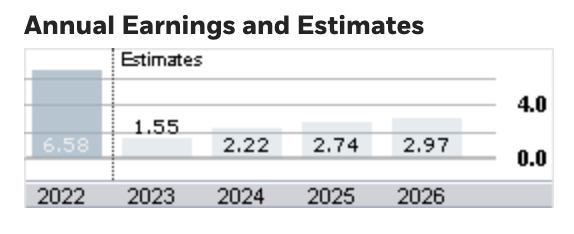

The estimates here tell a story of revenue and earnings falling SHARPLY, and growing from 2024 on, but so slowly that we don’t even get anywhere near 2022 levels over the next 3 years.

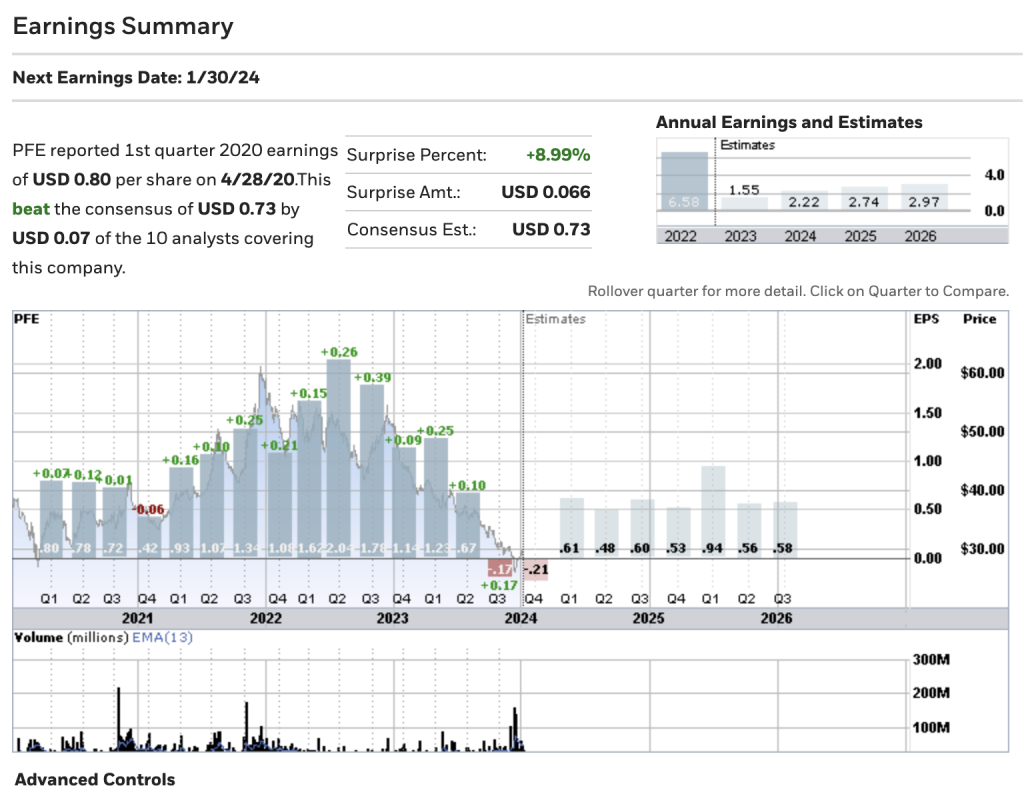

I’m going to include the full earnings chart from Etrade, mostly just to show how PFE earnings have surprised to the upside almost every quarter, sometimes by as much as 25%, all while the stock continued to slide down. I mean the numbers were horrible… but not as horrible as the analysts expected, which maybe points to some strong management. We’ll reserve judgement for now.

The next earnings call is January 30, which will lock in the numbers for the 2023 fiscal year for them. There’s likely to be a big move up or down around earnings, which I’d rather avoid, but if we want to load up now before the market rotates from tech into healthcare and other sectors we may have to buy sooner than later.

It’s kind of useful to think a little more about price to earnings ratios. While looking PEs up, you might notice different numbers on different websites. Some will show the 12 month “trailing PE”, some will show the 12 month “forward PE”, and depending on which numbers and estimates the PE was calculated from you might get something in between. So e.g. if we take the current stock price of $29.58 and divide by Etrade’s aggregate estimate (note that 3 out of 4 quarters are already reported, so the estimate is likely to be fairly close) of $1.55, we get a PE of 19, which is less good than the 16 PE Etrade reports right now.

So in short, in 22 days or so, new earnings numbers are going to come out, and the PE ratio for PFE will update, and anyone trading the stock based on that ratio will react accordingly. These ratios are most useful when you track their change over time. Don’t get too caught up on the specific value at any given time for one specific ratio.

Here’s a good piece from last February in the Financial Times by Jamie Smyth. The headline is “Pfizer pins hopes on record pipeline to recover from post-Covid hangover.” Here are some of the interesting tidbits I got from this article, all worth following up on:

“Pfizer expects sales of Comirnaty, the Covid vaccine it developed with German company BioNTech, and its antiviral pill Paxlovid, to fall 62 per cent to $21.5bn in 2023, compared to last year.”

Holy shit! Falling 62% to $21.5B. I’m catching up here to realize that A LOT of Pfizer’s revenues in 2022 were COVID related. At least $35B+ (1/3 the $100B total) came from these two drugs. How diversified is Pfizer really? I still haven’t dug into an actual earnings calls, but something I will look for is a breakdown of their revenue by drug or at least group.

More patent news, the article suggests the loss of exclusivity on cancer medicines Xtandi and Ibrance could “blow an additional $17bn hole in annual revenues by 2030.” That’s a long ways out. So plenty of time to work around it, but $17b is about 1/3 the 2023 estimated revenue.

This quote was also interesting:

Instead, since becoming chief executive in 2019, Albert Bourla, has sought to transform the company from a diversified pharmaceutical conglomerate into a nimbler, science-led business.

I’ll hope to find out more about what that really means and if that’s just PR speak or something that is really driving Bourla and the company.

This post is getting long, so I’m going to cut it off here. I also need some time to listen to those earnings calls and parse what I find there. I’ll look to get this series finished well before the Jan 30 earnings call.