Microsoft (MSFT) at $378: Accumulating the AI Operating System at a Discount

Microsoft is down 32% from its August 2025 peak. At $379, you’re buying one of the best businesses ever built — triple-moat, 46% operating margins, 18% revenue growth — at a PEG of 1.22. That’s not a distressed company. That’s macro rotation hitting a blue chip.

The Business

Microsoft has three durable moats working in tandem:

- Switching costs — once a company is on Azure, Microsoft 365, and Teams, the migration cost is measured in years, not months

- Network effects — GitHub (100M+ developers), LinkedIn (1B+ members), Teams integrations

- Scale — $318B revenue, 68% gross margins, $37B free cash flow

Satya Nadella’s 12-year cloud pivot is one of the best CEO transformation stories in tech. LinkedIn ($26B), GitHub ($7.5B), and OpenAI ($13B+) all look prescient in hindsight. The capital allocation discipline shows up in the numbers: 20% payout ratio, aggressive buybacks, and margin expansion while scaling aggressively.

The AI Thesis

Microsoft is building the operating system for the AI era across three layers:

- Azure — AI infrastructure. Competing directly with AWS and Google Cloud, growing ~22% YoY, and the preferred deployment platform for OpenAI workloads.

- Microsoft 365 Copilot — Enterprise AI productivity. The $30/user/month add-on on top of the existing 400M+ O365 user base is the largest enterprise software expansion opportunity in a decade.

- GitHub Copilot — Developer AI. Already the dominant AI coding tool; expanding into enterprise CI/CD and security.

The math on Copilot adoption is simple. Even 10% attach on 400M users at $30/month is $14B ARR from one product line. At 20% attach it’s $29B. These are incremental, high-margin revenue dollars on infrastructure Microsoft already owns.

Valuation

| Metric | Value | Note |

|---|---|---|

| Price | $379.40 | As of 2026-06-19 |

| Trailing P/E | 22.6x | Cheap vs. mega-cap peers |

| Forward P/E | 19.5x | On 18% growth |

| PEG | 1.22 | Fair for this compounder |

| P/S | 8.82x | High but justified by margins |

| Analyst Target | $561 | 55 analysts, Strong Buy consensus |

Not cheap by absolute standards. But cheapest in the mega-cap AI peer group, and down 32% from peak. The selloff is sector/macro rotation — the revenue growth and margin expansion story is intact.

EPS likely reaches $28–35+ by FY2029-2030. At 20x earnings (conservative for Microsoft), that’s $560–700 fair value. At the current $379, the setup is compelling on a 3-5 year horizon.

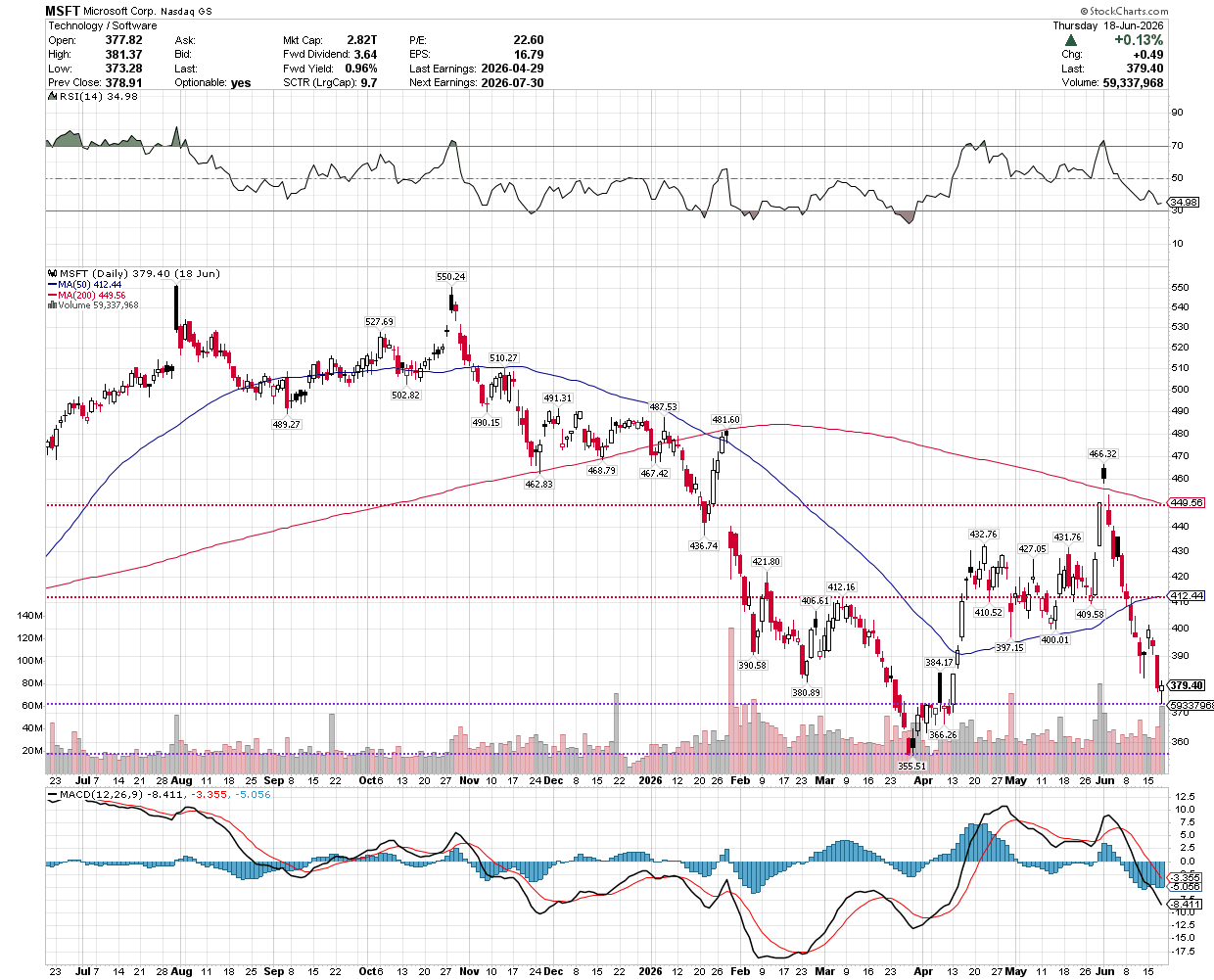

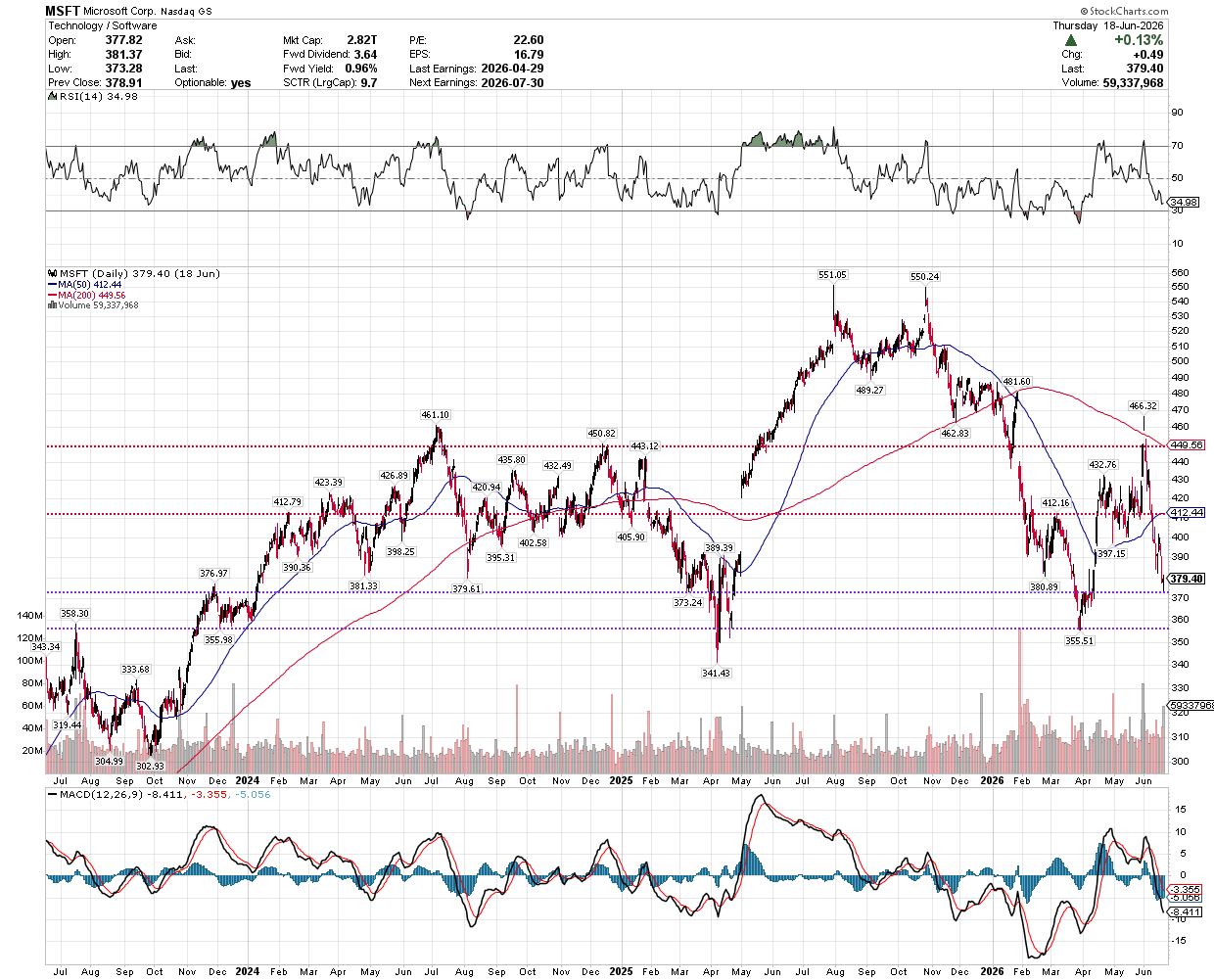

Technical Picture

The honest read: full downtrend. Price is 8% below the 50 DMA ($412) and 16% below the 200 DMA ($449). Death cross in place. MACD still falling, no crossover.

Key levels to watch:

- $356 — April 2026 52-week low; the floor. Hold or break, this is the line.

- $373 — Recent intraday low; tested and held. Immediate support.

- $390–400 — 2024 consolidation zone; major base before the 2025 breakout.

- $412 — 50 DMA; first resistance, trend confirmation if reclaimed.

- $449 — 200 DMA; major overhead resistance.

RSI is at 35 — approaching oversold, not there yet. No reversal signal, but the selling pressure is exhausting.

The Risk

One real risk worth naming: AI capex ROI. Microsoft is spending $80B+ annually on AI infrastructure. If Azure AI revenue doesn’t accelerate materially in FY2027, the capex story looks broken and multiples compress further. Google Cloud is growing faster (28% vs Azure’s ~22%) — that’s a secondary concern for Azure’s moat durability.

Next earnings: July 30, 2026. Azure growth rate is the key metric. Consensus is $4.24/share.

The Play

For a 3-5 year framework, the $355–380 zone is accumulation territory. The fundamental thesis is intact. The 32% drawdown is macro, not structural.

Strategy: size in layers. First tranche here at current levels. Add if it tests the April low ($356). Hold for the 50 DMA reclaim ($412) as trend confirmation — that’s when the technical picture starts cooperating with the fundamental one.

Not financial advice. Do your own due diligence.