SiriusXM closed today at $27.52, up 52% from its December lows and trading above both its 50-day and 200-day moving averages for the first time in years. The market is re-rating this stock from “terminal decline” to “value with optionality.” The question is whether that re-rating is real — or whether you’re buying a melting ice cube at a slightly higher price.

I ran a full research package on SIRI this week. Here’s what I found.

Charts

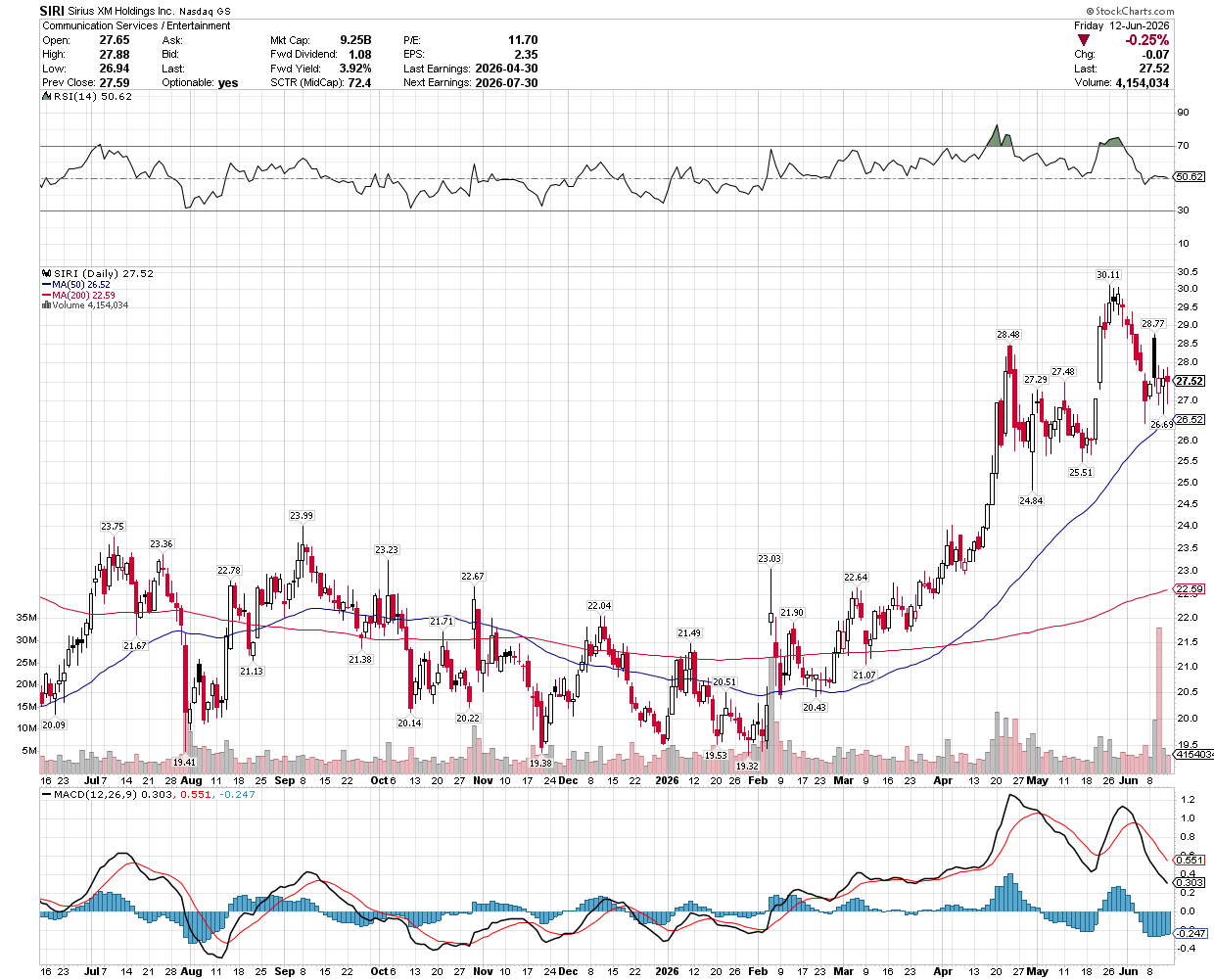

1-Year Daily

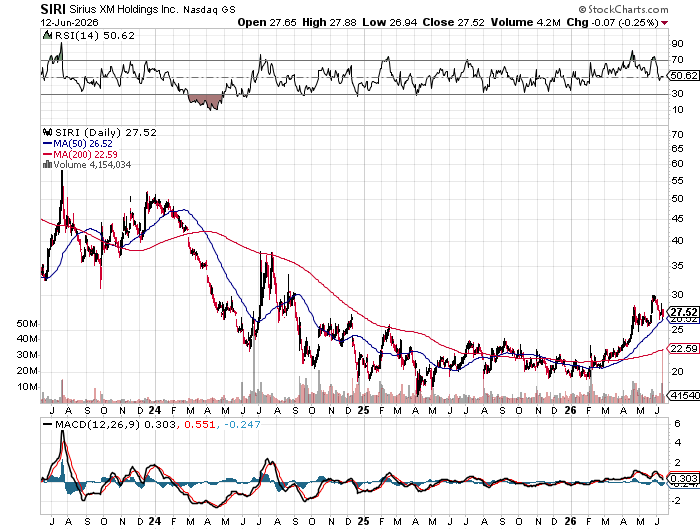

3-Year Daily

The business in one paragraph

SiriusXM is satellite radio plus Pandora streaming. ~$8.6B in revenue, ~$846M in profit, 47% gross margins, 22% operating margins. The content moat is real — Howard Stern, live sports, exclusive talk — but the structural challenge is equally real: streaming competition from Spotify and Apple Music is eating the addressable market from the bottom up. Revenue grew 1.1% last year. That’s not growth. That’s treading water.

Why the stock moved

SIRI just broke a multi-year downtrend. From December 2025 through May 2026, the stock rallied from the low $18s to a peak of $30.11 — a 52% move. It’s currently pulling back ~8% from that peak, which is healthy consolidation, not a reversal.

The key technical levels:

| Level | Price | Significance |

|---|---|---|

| 52-week high | $30.11 | Recent peak, strong resistance |

| Overhead resistance | $28.46 | Tested multiple times |

| Recent support | $26.53 | First line of defense on pullbacks |

| Breakout level | $24.46 | Major breakout from the base |

| 200 DMA | $22.59 | Long-term floor |

RSI is at 60 — neutral, with room to run. MACD is showing some bearish divergence after the May peak but remains above zero. The 200 DMA sits at $22.59, and price is well above it. This is the first time in years SIRI has been above both key moving averages simultaneously. That’s a trend reversal signal worth respecting.

The bull case: three paths to upside

SIRI is a value play with three distinct possible outcomes:

1. Liberty Media takes it private. John Malone’s Liberty Media owns a big stake. Malone is patient, value-focused, and has a long track record of extracting value from media companies through spinoffs, tracking stocks, and take-privates. If SIRI stays cheap long enough, Malone has every incentive to take the remaining public float private at a premium. This is the “smart money” catalyst — you don’t bet against Malone in media.

2. The streaming pivot works. Pandora gives SIRI a streaming foothold. If they can stabilize subscriber losses by converting satellite radio customers into streaming customers (and capture the ones who were going to leave anyway), margins expand. Streaming doesn’t require satellite infrastructure spend. The math is simple: if Pandora stops the sub bleed, the cash flow story gets much better.

3. Slow-shrink capital return. Even if neither of the above happens, SIRI is a cash machine that returns capital aggressively. The dividend yield is 3.9% and buybacks are ongoing. If the business shrinks at 2-3% per year but returns 6-7% in dividends and buybacks, you’re getting paid to hold a slowly declining asset. That’s not exciting, but it’s not a disaster either — and the market is pricing in something worse than that.

The bear case: why it might be a value trap

The risk is simple: satellite radio is a declining technology, and the decline could accelerate.

- Subscriber losses. Every quarter that SIRI loses net subscribers, the “value” part of the value play erodes. Cheap multiples don’t matter if the denominator (earnings) is shrinking.

- Debt. Debt-to-equity is 84.9. That’s high. If growth doesn’t return and interest rates stay elevated, the debt burden becomes a real problem. A structurally declining business with high debt is the textbook value trap profile.

- Streaming isn’t a moat. Pandora is not Spotify. It’s not Apple Music. SIRI’s streaming position is weak relative to the pure-play streamers. The “streaming pivot” thesis assumes they can compete where they’ve historically been second-tier.

The worst case: SIRI is the next print media — a business that generates cash but shrinks every year until the cash flow turns negative. At that point, the dividend gets cut, the buybacks stop, and the stock re-rates lower permanently.

Valuation: cheap for a reason?

| Metric | SIRI | Benchmark |

|---|---|---|

| P/E | 11.7 | ~15 |

| P/S | 1.1 | ~2x |

| Dividend Yield | 3.9% | ~1.5% |

| D/E | 84.9 | < 50 |

The multiples are cheap. But cheap multiples on a no-growth business are not the same as cheap multiples on a growth business. SIRI trades at a discount because the market doesn’t believe the earnings are sustainable. If they are — if SIRI can hold subs flat or grow even modestly — the stock is meaningfully undervalued. If they aren’t, the stock is fairly priced for a slow decline.

Where I’d look to add

If you believe the SIRI thesis, the entry points matter:

- $26.53 — recent support, the first place buyers stepped in during the pullback

- $24.46 — the breakout level from the base, a critical retest zone

- $22.59 — the 200 DMA, the long-term floor. If it breaks below this, the trend reversal thesis is broken and you need to reassess

Buying at $27.52 (current price) means you’re buying into strength after a 52% rally. That’s not ideal. Patience — waiting for a pullback to one of the levels above — gives you a better risk/reward.

The bottom line

SIRI is a cheap, cash-generative legacy media business trying to avoid becoming a melting ice cube. The stock just broke a multi-year downtrend and the market is re-rating it from “terminal decline” to “value with optionality.” The 3.9% dividend yield pays you to wait while management figures out if the streaming pivot works or Liberty Media makes a move.

This is not a growth story. This is not a tech story. This is a value play on a structurally challenged business with smart money (Malone) involved. Size accordingly. Watch subscriber trends and Liberty’s next move.

If SIRI holds above $26.53 and stabilizes, the re-rating has legs. If it breaks below $22.59, the reversal is dead and the melting ice cube thesis wins.

Not financial advice. Do your own due diligence.